How to enroll in the Medicare GLP-1 Bridge

Medicare covers GLP-1s for $50/month starting July 1, but patients don’t sign up directly. Instead their doctor needs to fax in a prior authorization form for the bridge.

This post describes what patients should know about eligibility for the Medicare’s GLP-1 Bridge program. It covers how the Bridge actually gets turned on, whether you’re likely to qualify, what to bring to your doctor to speed things up, and what happens at the pharmacy. For the full policy background (why the Bridge exists, how long it lasts, how it fits with Medicare’s other GLP-1 coverage), see Medicare covers GLP-1s for $50/month.

You check eligibility and talk to your doctor. Your doctor handles the prior authorization. The pharmacy charges a fixed $50 monthly copay.

You check eligibility and talk to your doctor. Your doctor handles the prior authorization. The pharmacy charges a fixed $50 monthly copay.

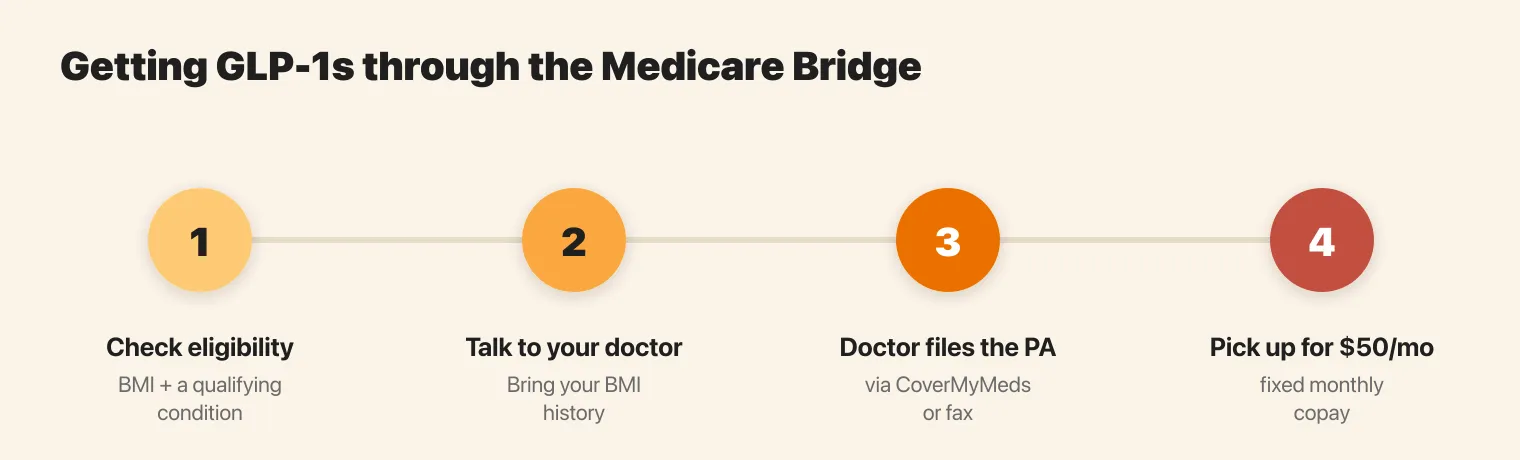

How do you sign up for the Medicare GLP-1 Bridge?

You don’t sign up directly, and that’s by design. Submission is restricted to prescribing clinicians, so the work happens in your doctor’s office. The sequence looks like this:

- Your pharmacy runs a claim that gets denied. Bridge drugs route through a dedicated billing channel. The first claim is expected to come back denied, which is what tells the system a Bridge prior authorization is needed. This is a normal step, not a rejection of your coverage.

- Your doctor submits the prior authorization. They complete the CMS GLP-1 Bridge form and send it electronically (through CoverMyMeds) or by fax. The form asks for your BMI at the time you started a GLP-1 and which qualifying conditions you have.

- You fill the prescription for $50. Once approved, you pay a fixed $50 copay per monthly supply.

So your job is really steps you do with your doctor: confirm you’re eligible, and give them the information they need to fill out the form correctly the first time.

Are you eligible for the GLP-1 Bridge?

The Bridge covers GLP-1s prescribed for weight loss when you’re 18 or older and meet a BMI threshold paired with the right condition:

| Your BMI | What else you need |

|---|---|

| 35 or higher | Nothing else required |

| 30 or higher | Heart failure with preserved ejection fraction, uncontrolled high blood pressure, or chronic kidney disease (stage 3a or higher) |

| 27 or higher | Pre-diabetes, a prior heart attack, a prior stroke, or symptomatic peripheral artery disease |

BMI is measured at the point you started a GLP-1, not where you are today. If you began semaglutide two years ago at a BMI of 37 and you’re now at 32, you still qualify. The full eligibility rules, including how the Bridge interacts with Medicare’s existing coverage for diabetes and cardiovascular disease, are in the main coverage post.

What to bring to your doctor

The prior authorization goes faster when your doctor has the answers the form wants. Before your visit, gather:

- Your starting BMI. The weight and height from when you first began a GLP-1, if you’ve been on one. If you’re starting fresh, your current numbers.

- Your qualifying conditions. Pre-diabetes, prior heart attack or stroke, peripheral artery disease, heart failure, kidney disease, or blood pressure readings on your current medications.

- Your current medications, especially blood pressure drugs, since uncontrolled hypertension is defined as readings above 140/90 despite two of them.

Several of these conditions are confirmed by lab work rather than symptoms. Pre-diabetes, chronic kidney disease, and the markers behind cardiovascular risk often show up on a blood panel before you’d notice anything.

What does the GLP-1 Bridge cost?

You pay $50 per monthly supply, and that amount doesn’t change based on where you are in your Part D benefit. It’s worth knowing that the $50 does not count toward your Part D out-of-pocket cap, and manufacturer coupons can’t be applied to Bridge claims. For comparison, cash prices for these drugs usually run $1,000 to $1,400 a month. The cost details are covered in full in the coverage post.

Why was my pharmacy claim denied first?

Because the system is built that way. The denied claim is the trigger that tells Medicare a Bridge prior authorization should be created. If your pharmacist tells you the first claim came back denied, that’s the process working, not a sign you’ve been turned down. Your doctor’s prior authorization is the next step, and it’s what actually opens coverage.

If you want the clinical detail (which 12 questions are on the form, how your provider submits it, and what holds up an approval), we wrote a companion piece for clinicians: the Medicare GLP-1 Bridge prior authorization form, explained.

This post is part of our series on Medicare coverage for cardiovascular health. See also: Medicare covers GLP-1s for $50/month and the GLP-1 Bridge prior authorization form.

Get your free 30-day heart health guide

Evidence-based steps to optimize your heart health.